by John Nyiszter | May 4, 2023 | condo owners, condos, First Time Home Buyers, FSBO, Home Owners, Home Sellers, investment properties, luxury homes, townhome owners, Uncategorized

How Homeowners Win When They Downsize

Downsizing has long been a popular option when homeowners reach retirement age. But there are plenty of other life changes that could make downsizing worthwhile. Homeowners who have experienced a change in their lives or no longer feel like their house fits their needs may benefit from downsizing too. U.S. News explains:

“Downsizing is somewhat common among older people and retirees who no longer have children living at home. But these days, younger people are also looking to downsize to save money on housing . . .”

And when inflation has made most things significantly more expensive, saving money where you can has a lot of appeal. So, if you’re thinking about ways to budget differently, it could be worthwhile to take your home into consideration.

When you think about cutting down on your spending, odds are you think of frequent purchases, like groceries and other goods. But when you downsize your house, you often end up downsizing the bills that come with it, like your mortgage payment, energy costs, and maintenance requirements. Realtor.com shares:

“A smaller home typically means lower bills and less upkeep. Then there’s the potential windfall that comes from selling your larger home and buying something smaller.”

That windfall is thanks to your home equity. If you’ve been in your house for a while, odds are you’ve developed a considerable amount of equity. Your home equity is an asset you can use to help you buy a home that better suits your needs today.

And when you’re ready to make a move, your team of real estate experts will be your guides through every step of the process. That includes setting the right price for your house when you sell, finding the best location and size for your next home, and understanding what you can afford at today’s mortgage rate.

What This Means for You

If you’re thinking about downsizing, ask yourself these questions:

- Do the original reasons I bought my current house still stand, or have my needs changed since then?

- Do I really need and want the space I have right now, or could somewhere smaller be a better fit?

- What are my housing expenses right now, and how much do I want to try to save by downsizing?

Once you know the answers to these questions, meet with a real estate advisor to get an answer to this one: What are my options in the market right now? A local housing market professional can walk you through how much equity you have in your house and how it positions you to win when you downsize.

Bottom Line

If you’re looking to save money, downsizing your home could be a great help toward your goal. Let’s connect to talk about your goals in the housing market this year.

by John Nyiszter | May 2, 2023 | condo owners, condos, First Time Home Buyers, FSBO, Home Owners, Home Sellers, investment properties, luxury homes, townhome owners

What’s the Difference Between a Home Inspection and an Appraisal?

If you’re planning to buy a home, an inspection is an important step in the process. It assesses the condition of the home before you finalize the transaction. It’s also a different step in the process from an appraisal, which is a professional evaluation of the market value of the home you’d like to buy. In most cases, an appraisal is ordered by the lender to confirm or verify the value of the home prior to lending a buyer money for the purchase. Here’s the breakdown of each one and why they’re both important when buying a home.

Home Inspection

Here’s the key difference between an inspection and an appraisal. Bankrate says:

“In short, while an appraisal helps you understand a home’s value, inspections help you understand a home’s condition.”

The home inspection is a way to determine the current state, safety, and condition of the home before you finalize the sale. If anything is questionable in the inspection process – like the age of the roof, the state of the HVAC system, or just about anything else – you as a buyer have the option to discuss and negotiate any potential issues or repairs with the seller before the transaction is final. Your real estate agent is a key expert to help you through this part of the process.

Home Appraisal

The National Association of Realtors (NAR) explains:

“A home purchase is typically the largest investment someone will make. Protect yourself by getting your investment appraised! An appraiser will observe the property, analyze the data, and report their findings to their client. For the typical home purchase transaction, the lender usually orders the appraisal to assist in the lender’s decision to provide funds for a mortgage.”

When you apply for a mortgage, an unbiased appraisal (which is required by the lender) is the best way to confirm the value of the home based on the sale price. Regardless of what you’re willing to pay for a house, if you’ll be using a mortgage to fund your purchase, the appraisal will help make sure the bank doesn’t loan you more than what the home is worth.

This is especially critical in today’s sellers’ market where low inventory is driving an increase in bidding wars, which can push home prices upward. When sellers are in a strong position like this, they tend to believe they can set whatever price they want for their house under the assumption that competing buyers will be willing to pay more.

However, the lender will only allow the buyer to borrow based on the value of the home. This is what helps keep home prices in check. If there’s ever any confusion or discrepancy between the appraisal and the sale price, your trusted real estate professional will help you navigate any additional negotiations in the buying process.

Bottom Line

The inspection and the appraisal are critical steps when buying a home, and you don’t need to manage them by yourself. Let’s connect today so you have the expert guidance you need to navigate the entire homebuying process.

by John Nyiszter | May 2, 2023 | condo owners, condos, First Time Home Buyers, FSBO, Home Owners, Home Sellers, investment properties, luxury homes, townhome owners

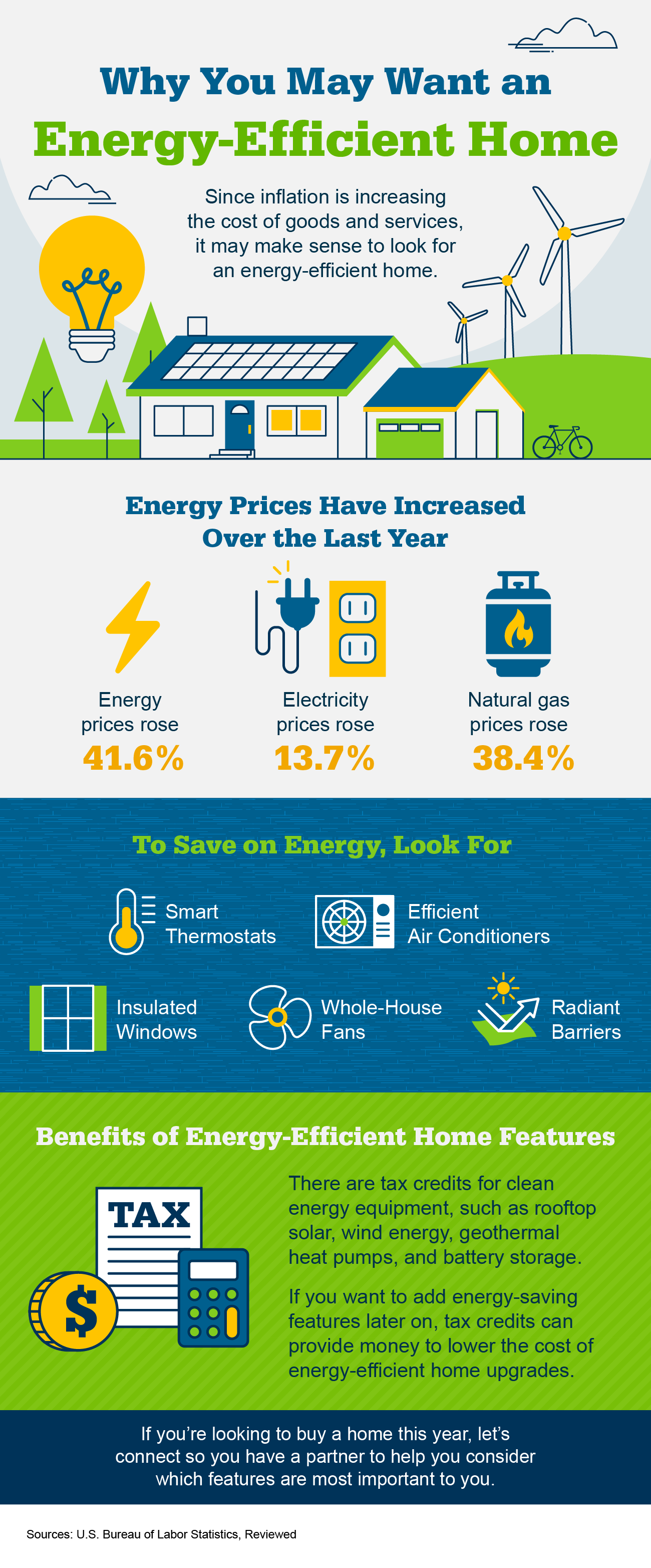

Why You May Want an Energy-Efficient Home [INFOGRAPHIC]

Some Highlights

- Since inflation is increasing the cost of goods and services, it may make sense to look for an energy-efficient home.

- Energy prices have increased over the last year, so look for energy-efficient features in your home search.

- If you’re looking to buy a home this year, let’s connect so you have a partner to help you consider which features are most important to you.

by John Nyiszter | May 2, 2023 | condo owners, condos, First Time Home Buyers, FSBO, Home Owners, Home Sellers, investment properties, luxury homes, townhome owners

The Power of Pre-Approval

If you’re buying a home this spring, today’s housing market can feel like a challenge. With so few homes on the market right now, plus higher mortgage rates, it’s essential to have a firm grasp on your homebuying budget. You’ll also need a sense of determination to find the right house and act quickly when you go to put in an offer. One thing you can do to help you prepare is to get pre-approved.

To understand why it’s such an important step, you need to know what pre-approval is. As part of the process, a lender looks at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand how much money you can borrow.

Freddie Mac explains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand how much you may be able to borrow so you have a stronger grasp of your options. And with higher mortgage rates impacting affordability for many buyers today, a solid understanding of your numbers is even more important.

Pre-Approval Helps Show You’re a Serious Buyer

That’s not the only thing pre-approval can do. Another added benefit is it can help a seller feel more confident in your offer because it shows you’re serious about buying their house. And, with sellers seeing a slight increase in the number of offers again this spring, making a strong offer when you find the perfect house is key.

As a recent article from the Wall Street Journal (WSJ) says:

“If you plan to use a mortgage for your home purchase, preapproval should be among the first steps in your search process. Not only can getting preapproved help you zero in on the right price range, but it can give you a leg up on other buyers, too.”

Bottom Line

Getting pre-approved is an important first step when you’re buying a home. It lets you know what you can borrow for your loan and shows sellers you’re serious. Connect with a local real estate professional and a trusted lender so you have the tools you need to purchase a home in today’s market.

by John Nyiszter | May 2, 2023 | condo owners, condos, First Time Home Buyers, FSBO, Home Owners, Home Sellers, investment properties, luxury homes, townhome owners

What Are the Experts Saying About the Spring Housing Market?

The housing market’s been going through a lot of change lately, and there’s been uncertainty surrounding what will happen this spring. You may be wondering if more homes will go on the market, what’s next with home prices and mortgage rates, or what the best advice is for someone in your position right now.

Here’s what industry experts are saying right now about the spring housing market and what it means for you:

Selma Hepp, Chief Economist, CoreLogic:

“We see more competition among buyers . . . Housing supply also tends to grow during the spring months. And this is also the time of year when relatively more migration happens, as people graduate and move elsewhere looking for jobs.”

Greg McBride, Chief Financial Analyst, Bankrate:

“I don’t expect big moves in prices in the span of a month, but like the flower buds of spring, the housing market is showing signs of improvement. A pick up in activity with inventory still low does bode well for home prices.”

Rick Sharga, Founder and CEO, CJ Patrick Company:

“If you can find a home you love and can afford at today’s prices, don’t wait. Home prices in most of the country are unlikely to crash, and mortgage rates will only come down very gradually if they decline at all this year.”

Jeff Tucker, Senior Economist, Zillow:

“The market is still much friendlier this spring for buyers who can overcome affordability hurdles, but buyers are going to see more competition than they might expect because there are not many homes on the market to go around. New listings are increasing, which they almost always do this time of year, but not nearly as quickly as usual.”

Bottom Line

If you’re thinking about selling your house, this spring’s a great time to do so while inventory is still so low. And if you’re in a good position to buy, lean on your team of expert advisors for the best advice. Whatever your plans, let’s connect to make sure you’re able to navigate the spring housing market with confidence.

by John Nyiszter | May 2, 2023 | condo owners, condos, First Time Home Buyers, FSBO, Home Owners, Home Sellers, investment properties, luxury homes, townhome owners

The Three Factors Affecting Home Affordability Today

There’s been a lot of focus on higher mortgage rates and how they’re creating affordability challenges for today’s homebuyers. It’s true that rates climbed dramatically since the record-low we saw during the pandemic. But home affordability is based on more than just mortgage rates – it’s determined by a combination of mortgage rates, home prices, and wages.

Considering how each one of these factors is changing gives you the full picture of home affordability today. Here’s the latest.

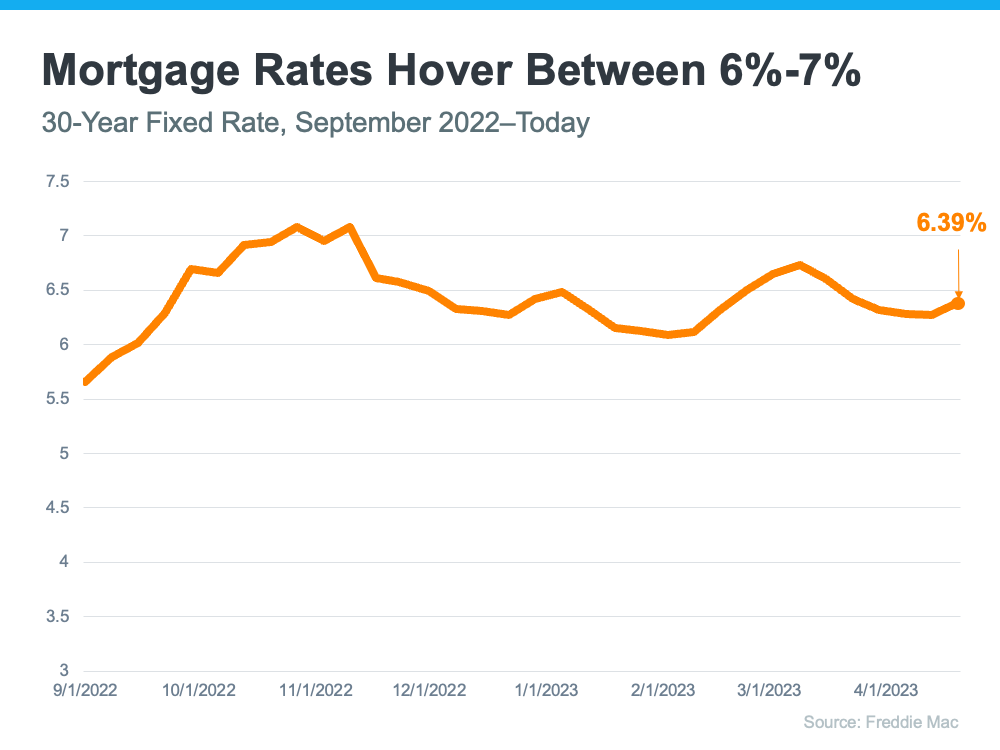

1. Mortgage Rates

While mortgage rates are higher than they were a year ago, they’ve hovered primarily between 6% and 7% for nearly eight months now (see graph below):

As the graph shows, mortgage rates have experienced some volatility during that time. And even a small change in mortgage rates impacts your purchasing power. That’s why it’s so important to lean on your team of real estate professionals for expert advice to stay up to date on what’s happening in the market. While it’s hard to project where mortgage rates will go from here, many experts agree they’ll likely continue to remain around 6%-7% in the immediate future.

2. Home Prices

Over the past few years, home prices appreciated rapidly as the record-low mortgage rates we saw during the pandemic led to a surge in buyer demand. The heightened buyer demand happened while the supply of homes for sale was at record lows, and that imbalance put upward pressure on home prices. However, today’s higher mortgage rates have slowed down price appreciation.

And, the truth is, home price appreciation varies by market. Some areas are seeing slight declines while others have prices that are climbing. As Selma Hepp, Chief Economist at CoreLogic, explains:

“The divergence in home price changes across the U.S. reflects a tale of two housing markets. Declines in the West are due to the tech industry slowdown and a severe lack of affordability after decades of undersupply. The consistent gains in the Southeast and South reflect strong job markets, in-migration patterns and relative affordability due to new home construction.”

To find out what’s happening with prices in your local market, reach out to a trusted real estate agent.

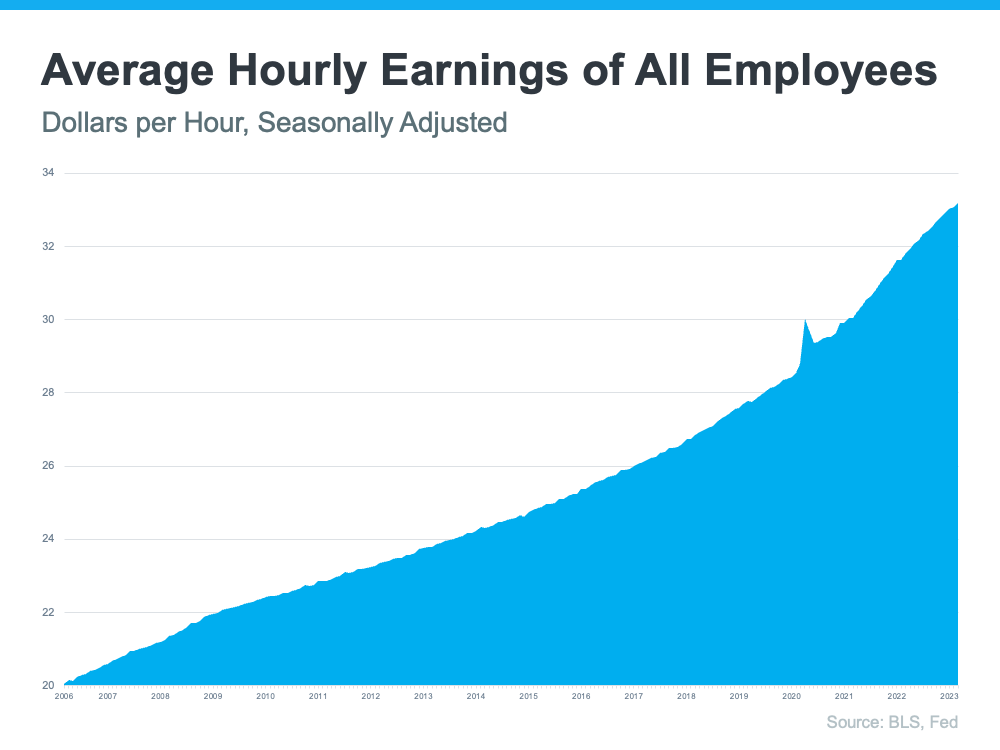

3. Wages

The most positive factor in affordability right now is rising income. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time:

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage since you don’t have to put as much of your paycheck toward your monthly housing cost.

Home affordability comes down to a combination of rates, prices, and wages. If you have questions or want to learn more, reach out to a real estate professional who can explain what’s happening locally and how these factors work together.

Bottom Line

If you’re planning to buy a home, knowing the key factors that impact affordability is important so you can make an informed decision. To stay up to date on the latest on each, let’s connect today.